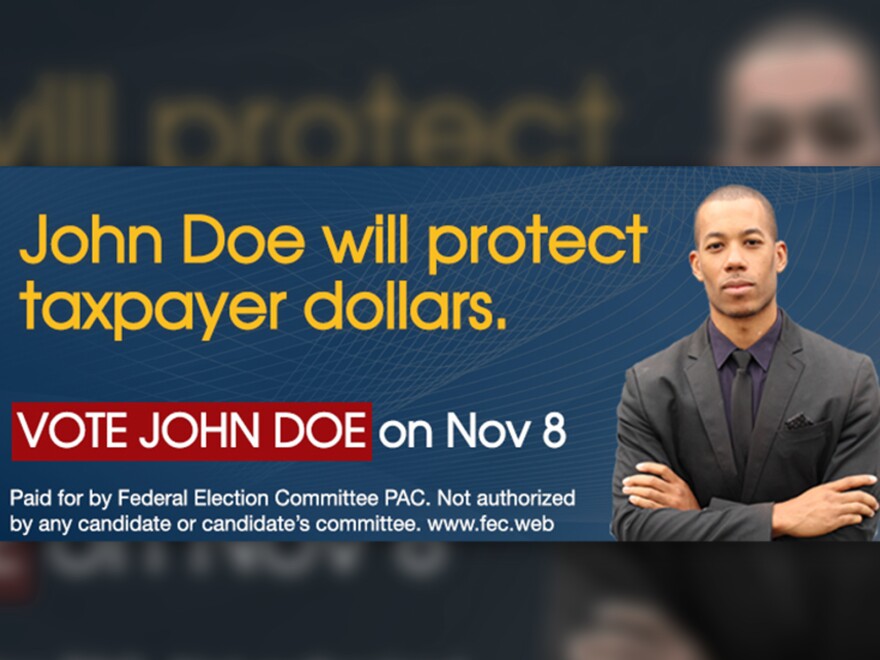

You are watching a mid-October football game, and a grim voice tells you a candidate “voted to cut benefits” or “raised your taxes.” The group paying for the ad has a forgettable name, a Washington mailing address, and a required line at the end: “Paid for by….”

Sometimes the sponsor is a Super PAC. Sometimes it is a nonprofit “social welfare” group. And sometimes it is a 527 organization, a creature of tax law that exists mainly to influence elections, raise large sums quickly, and leave a paper trail that is both real and easy to miss if you do not know where to look.

This is Section 527 in plain English: what it is, how it fits into election law, what it must disclose, and why you keep seeing its ads.

Join the Discussion

What a 527 organization is

A “527” is named for Section 527 of the Internal Revenue Code. It is a tax category for “political organizations” that are organized and operated primarily to accept contributions or make expenditures for an exempt function, meaning influencing the selection, nomination, election, or appointment of individuals to public office.

Think of it as a political organization defined first by tax law, not by campaign law. That status is about tax treatment and IRS filing rules. It is not a blanket permission slip to ignore federal or state campaign rules.

A 527 can be created for many political purposes, including:

- Supporting or opposing candidates through voter outreach and advertising

- Messaging about issues in ways that often intensify around election season

- Mobilizing voters through mail, texts, phone banks, and get-out-the-vote operations

The key idea is mission: a 527 exists to play in politics. It is not a charity that dabbles in politics. Politics is the point.

One practical note: contributions to 527s are generally not tax-deductible.

Why 527s exist: different rulebooks

Americans often assume “campaign finance” is one rulebook. It is not. It is several overlapping rulebooks.

Tax law decides what kind of organization you are for IRS purposes, how you are taxed, and what forms you file.

Election law, primarily enforced by the Federal Election Commission (FEC), decides when your spending counts as federal campaign activity, what reporting triggers apply, and what coordination limits exist when candidates and outside groups interact.

527s sit in the overlap. Some of them also function as political committees under federal law, which can mean FEC registration and reporting. Others operate in ways that keep them outside certain FEC definitions, especially when their activity is structured as nonfederal work or issue-focused messaging. “Issue advocacy” is not the tax test for 527 status, but it is a common label in the campaign finance world for communications that are designed to persuade without explicitly telling you how to vote.

This is why a 527 can feel both transparent and opaque at the same time. It may disclose donors, but to a different agency, on a different schedule, in forms most voters never read.

What 527s must disclose

When people ask, “Do 527s have to disclose donors?” the honest answer is: often yes, but you have to know where to look, and the answer can depend on whether the group is also reporting as an FEC committee.

IRS filing and disclosure

Many 527 organizations file with the IRS, and the two forms that matter most for regular people are:

- Form 8871: the notice of organization (basic registration information)

- Form 8872: periodic reports of contributions and expenditures (the money in and the money out)

In practice, that means disclosure can be:

- Real: donor names and amounts may appear in public filings

- Technical: data is often buried in filings rather than presented like a simple donor list on an ad

- Time-sensitive: Form 8872 reporting can be monthly or quarterly, and may include pre-election reporting. It is not always “after the fact,” but it can still feel late compared to the speed of ads and social media.

One important carve-out: if a 527 registers with the FEC as a federal political committee (including an independent-expenditure-only committee), it generally reports to the FEC and may not file the same periodic disclosure with the IRS on Form 8872.

FEC disclosure (sometimes)

If a 527’s activity makes it a federal political committee, it may need to register and report to the FEC. When that happens, disclosure looks more like what people expect from a campaign finance database.

Also, some communications can trigger federal reporting even without “magic words.” Two labels you will see in this space are independent expenditures and electioneering communications, each with its own rules and reporting hooks.

How 527 money becomes ads

Most voters experience campaign finance through one thing: advertising volume.

Here is the basic pipeline:

- Donors give to a political group

- The group spends on media buys, consulting, data, and get-out-the-vote operations

- You see the ad with a required disclaimer, but usually without context about the group’s funding network

527s are built for this environment. They can raise substantial money, hire professional political vendors, and flood the airwaves quickly.

And because the disclosure is not presented to you in the moment you are being persuaded, the ad can feel like it came from nowhere. That is not an accident. It is a feature of how modern political persuasion is structured: the message is immediate, the transparency is technical.

527s vs. Super PACs

Super PACs are the better-known outside spending vehicle. But “Super PAC” and “527” are not the same label, even though they often overlap.

Super PACs in one sentence

A Super PAC is an independent-expenditure-only political committee that can raise unlimited money and spend unlimited money independently of candidates and parties, and it must disclose donors through FEC reporting. It also cannot coordinate its spending with the candidates it supports.

The overlap that confuses people

Technically, many Super PACs are also 527 political organizations under the tax code. They are political by design, and they fit the IRS definition. In everyday conversation, though, journalists and voters often use “527” as shorthand for election-focused groups that are not operating as FEC-registered committees, meaning their disclosure may show up primarily in IRS filings instead of the FEC’s standard campaign finance dashboards.

Key differences people actually feel

- Where you look: Super PAC data is usually easiest to pull on FEC.gov. Many non-FEC 527 disclosures live in IRS political organization filings.

- How fast it shows up: FEC reporting tends to be more familiar to watchdog groups and journalists. IRS reporting can still be public, but it is easier for casual readers to miss.

Bottom line: if you are trying to understand a political ad’s funding source, identifying whether the sponsor is a Super PAC or a non-FEC 527 tells you which database and which reporting cadence to check.

527s vs. 501(c) nonprofits

Many Americans lump “nonprofits” together as if they are all charities. But the tax code has multiple nonprofit lanes, and they have very different political permissions.

501(c)(3): charities

501(c)(3) organizations are the classic charities: educational institutions, relief organizations, museums, many civic groups. Donations are typically tax-deductible for donors. The tradeoff is strict: they cannot support or oppose candidates, and their lobbying is limited.

501(c)(4): social welfare groups

501(c)(4) organizations can engage in some political activity, but their primary purpose must be social welfare. They sit at the center of “dark money” debates because they generally do not publicly disclose donors the way FEC-reporting political committees do, even though donors can sometimes be revealed indirectly through other filings or state rules.

527: political organizations

A 527 is politics-first. That clarity is why the category exists.

So why does the confusion persist? Because ads do not explain tax categories, and because groups can choose structures strategically. If a donor wants one kind of disclosure, one kind of activity, or one kind of regulatory friction, different entities provide different paths.

Issue ads and the line everyone fights over

The most contested ground in modern campaign finance is the line between issue advocacy and electioneering.

An ad can praise or attack a candidate without using “magic words” like “vote for” or “defeat.” It can air right before an election. It can be targeted to persuadable voters. It can function like a campaign ad in every practical sense while being framed as a message about “issues.”

This is where 527s often live: close to elections, close to candidates, and close to the edge of definitions that trigger different legal obligations. And even when an ad avoids express advocacy, other categories like electioneering communications or independent expenditures can still trigger reporting requirements.

None of this means every 527 is trying to evade rules. It means the system itself rewards groups that understand which rulebook they are in at any given moment.

So are 527s dark money?

“Dark money” is not a single legal term. It is a public label for political spending where the true funding sources are not readily visible to the public in the moment it matters.

Many 527s are not dark in the pure sense because they can disclose donors through IRS filings. But they can still feel dark because:

- the disclosure is indirect (you have to search for it)

- the disclosure is time-lagged compared to the speed of ads

- funding can move through multiple entities before it reaches the group paying for an ad

If you have ever tried to trace a political message back to a real person or business and ended up in a maze of committees, affiliates, and similar names, you have met the modern transparency problem. It is less about whether information exists and more about whether ordinary citizens can realistically use it.

Why disclosure is a balancing act

Campaign finance fights are rarely just about money. They are about two constitutional instincts that can collide.

- Political speech is protected. Spending money to amplify speech is often treated as part of that protection in modern doctrine.

- Transparency is also a democratic value. Disclosure can help voters evaluate credibility, detect corruption risks, and understand who is trying to influence their choices.

The Supreme Court has generally been receptive to disclosure requirements even while striking down some spending restrictions. But the details matter, and the boundaries get litigated constantly.

That is why 527s are a useful civics lens. They force you to see how a system can be simultaneously committed to speech and skeptical of regulation, while still claiming to value informed citizenship.

How to spot a 527 behind an ad

You do not need a law degree. You need a few habits.

1) Read the disclaimer line

The “Paid for by” statement tells you the legal sponsor. Write it down or screenshot it.

2) Search the exact name plus “Form 8871” or “Form 8872”

Many 527s can be located through IRS political organization filings. Exact spelling matters. If you find a Form 8871, you have likely found the entity. If you find a Form 8872, you have likely found the money trail.

3) Check whether it is also an FEC committee

Some groups file with both systems depending on activity, and some report primarily to the FEC instead of filing IRS periodic disclosure. If you find an FEC committee page, you may get more frequent and more standardized reports.

4) Look for vendor patterns

Even when donors are hard to identify quickly, spending patterns can show the group’s seriousness, strategy, and connections: media buyers, consultants, and recurring contractors.

The takeaway

527 organizations are not a loophole in the simplistic sense. They are a predictable result of a system that regulates politics through multiple channels: tax law, election law, and constitutional doctrine that treats political advocacy as protected speech.

If you want the practical answer to “why am I seeing these ads,” it is this: 527s are designed to collect political money and convert it into voter influence fast, with disclosure that exists but often sits one step removed from the ad itself.

Knowing what a 527 is does not tell you whether an ad is truthful. It tells you where to look next, which is the first step in being the kind of citizen the Constitution assumes you can be.