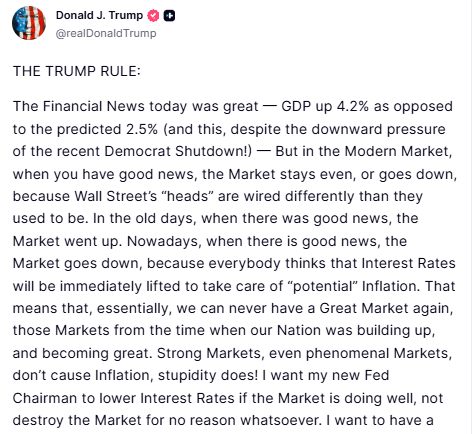

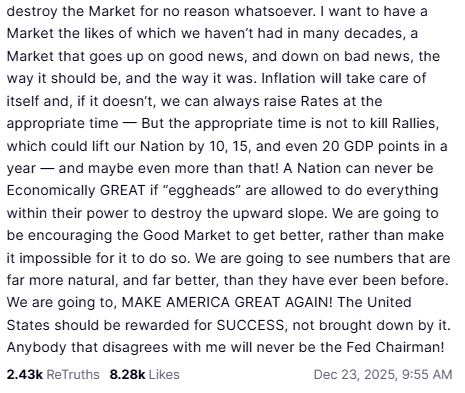

President Trump posted what he’s calling “THE TRUMP RULE” on Truth Social Tuesday morning: a 400-word manifesto declaring that the Federal Reserve should lower interest rates when the economy is doing well, not raise them.

The post claims GDP growth hit 4.2% against predictions of 2.5%. It argues that markets now go down on good news because investors expect rate hikes to combat inflation. And it concludes with a threat: “Anybody that disagrees with me will never be the Fed Chairman!”

There’s just one problem with Trump’s economic theory. Actually, there are about twelve problems, ranging from factual inaccuracies to fundamental misunderstandings of how monetary policy works to a direct assault on Federal Reserve independence that would violate the institutional norms protecting the central bank from political interference.

Let’s start with what’s factually wrong, then address what’s economically nonsensical, and finish with the constitutional crisis Trump is threatening if he gets what he wants.

Fact Check: The GDP Numbers Don’t Match Reality

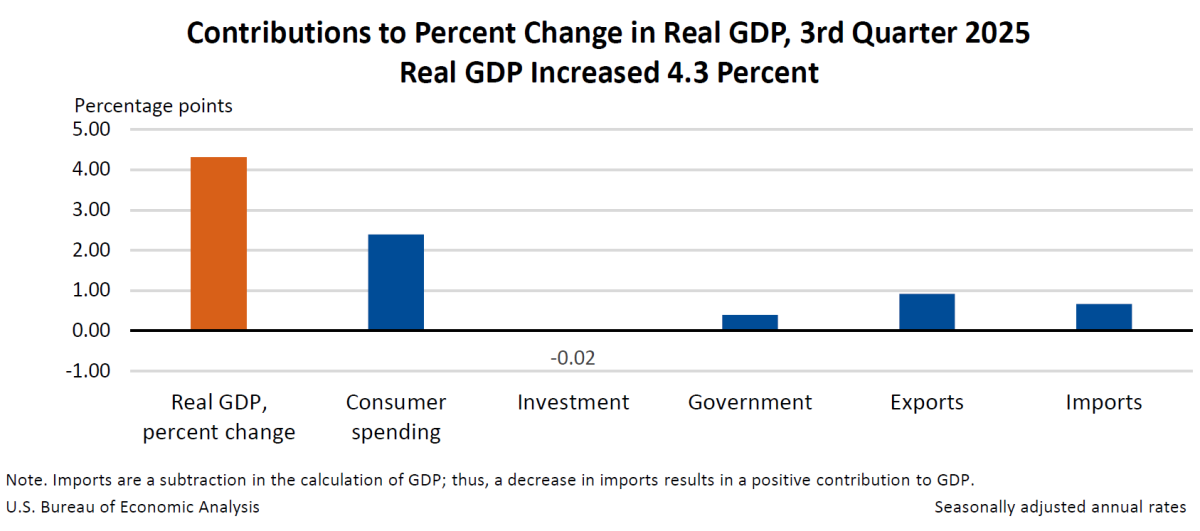

Trump claims GDP grew 4.2% “as opposed to the predicted 2.5%.” According to the Bureau of Economic Analysis, the most recent GDP data shows growth of 2.8% in the third quarter of 2025 – not 4.2%.

The 4.2% figure appears to be from the second quarter of 2018 during Trump’s first term. Either he’s confused about which numbers he’s reading, or he’s deliberately citing seven-year-old data while claiming it’s current.

The “predicted 2.5%” is also suspect. Consensus economist forecasts for Q3 2025 were closer to 2.0-2.3%, which means the actual 2.8% was indeed above expectations – but not by the dramatic margin Trump claims, and nowhere near the 4.2% he’s celebrating.

This matters because Trump’s entire argument rests on the economy performing spectacularly while markets remain flat. If GDP growth is actually modest rather than spectacular, his theory about market reactions to good news doesn’t apply to current conditions.

Fact Check: The “Democrat Shutdown” That Never Happened

Trump references “downward pressure of the recent Democrat Shutdown” as limiting GDP growth. There was no Democrat shutdown in 2025.

Congress passed a continuing resolution in September preventing a government shutdown, with bipartisan support in both chambers. The most recent actual shutdown was January 2018-2019 during Trump’s first term, when he demanded border wall funding – a shutdown that occurred when Republicans controlled the White House, Senate, and House.

Blaming Democrats for a shutdown that didn’t happen while celebrating GDP numbers from seven years ago suggests Trump is either working from severely outdated information or deliberately creating an alternate reality where his economic claims make sense.

How Markets Actually Respond to Economic News

Trump’s central claim is that “in the old days, when there was good news, the Market went up. Nowadays, when there is good news, the Market goes down, because everybody thinks that Interest Rates will be immediately lifted.”

This is partially correct but fundamentally misunderstands the relationship between economic indicators, monetary policy, and market behavior.

Markets don’t respond mechanically to “good news” or “bad news” – they respond to information about future conditions relative to current expectations. If GDP growth comes in higher than expected, markets must evaluate whether that growth is sustainable, whether it signals inflation pressure, and whether it will trigger Federal Reserve action that affects borrowing costs and corporate earnings.

Strong GDP growth combined with high inflation and rising unemployment (the current conditions) signals economic instability, not strength. Markets fall not because they’re “wired differently than they used to be,” but because investors recognize that growth accompanied by inflation and job losses isn’t sustainable prosperity – it’s overheating followed by likely contraction.

Trump wants markets to go up on good news regardless of context. But “GDP up 4.2%” matters less than whether that growth is inflationary, whether it’s concentrated in specific sectors, whether it’s sustainable, and whether it will require monetary policy responses that slow future growth.

The “old days” Trump references weren’t simpler times when markets mechanically rewarded good news. They were periods when inflation was lower, employment was stronger, and growth was more sustainable. Markets responded positively because the underlying conditions justified optimism. Current conditions don’t.

Why Central Banks Raise Rates During Growth

Trump argues that raising interest rates during strong economic performance “destroys the Market for no reason whatsoever.” This reveals a fundamental misunderstanding of what central banks do and why.

The Federal Reserve has a dual mandate: maximum employment and stable prices. When the economy grows too quickly, inflation typically follows as demand outpaces supply and labor markets tighten. The Fed raises interest rates to slow borrowing, reduce spending, and prevent inflation from spiraling out of control.

This isn’t “stupidity” – it’s the basic mechanism for managing business cycles. Without periodic rate increases to cool overheating, economies experience boom-bust cycles where rapid growth leads to unsustainable inflation, followed by sharp recessions that destroy wealth and employment.

Trump’s claim that “Inflation will take care of itself” contradicts everything economists know about inflation dynamics. Inflation doesn’t self-correct – it accelerates if left unchecked. The 1970s stagflation crisis resulted from precisely the approach Trump advocates: keeping rates low during inflationary periods and hoping inflation would resolve itself.

Paul Volcker finally broke that inflation cycle in the early 1980s by raising rates dramatically, triggering a recession but restoring price stability that enabled decades of subsequent growth. Trump apparently wants to reverse that lesson and return to the pre-Volcker approach that created the worst inflation crisis in modern American history.

The “10, 15, and Even 20 GDP Points” That Defy Reality

Trump claims his approach could “lift our Nation by 10, 15, and even 20 GDP points in a year — and maybe even more than that!”

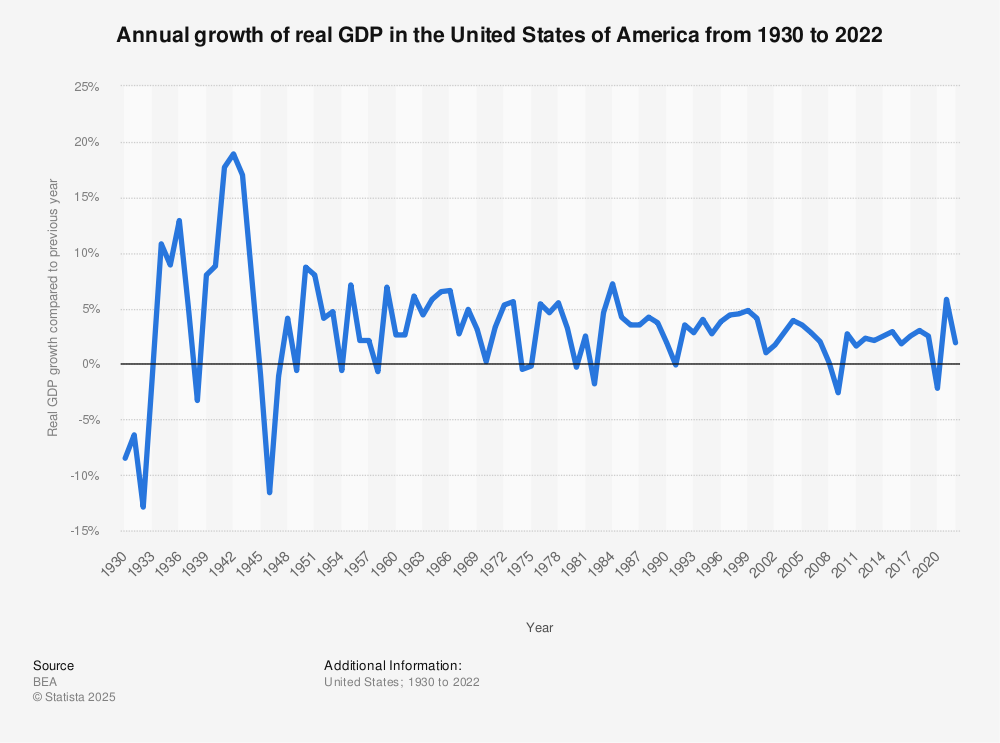

This is economically impossible. U.S. GDP growth hasn’t exceeded 7% in any year since 1984. China, during its fastest growth period, sustained 10-14% annual growth for limited periods before that pace became unsustainable. No developed economy has ever achieved 15-20% annual GDP growth outside of post-war rebuilding periods.

Trump appears to be confusing GDP growth rate with stock market point gains. The Dow Jones Industrial Average can gain hundreds or thousands of points in a year because it measures absolute price levels. GDP growth is a percentage measuring economic expansion.

Promising 20% GDP growth is like promising humans will start living to 200 years old because medical technology is improving. It’s not an optimistic projection – it’s detached from reality in ways that suggest either profound economic illiteracy or deliberate deception.

The Federal Reserve Independence Trump Wants to Destroy

The most constitutionally significant part of Trump’s post is the threat: “Anybody that disagrees with me will never be the Fed Chairman!”

The Federal Reserve was designed to be independent from political pressure precisely to prevent presidents from manipulating monetary policy for short-term political gain at the expense of long-term economic stability.

The President appoints the Fed Chair and Board of Governors, subject to Senate confirmation. But once appointed, Fed officials serve fixed terms and can’t be removed except for cause. This structure insulates monetary policy from political interference.

Trump’s declaration that he’ll only appoint Fed Chairs who agree with his economic theories eliminates that independence. If Fed officials must implement the President’s preferred policies to keep their jobs, they’re no longer independent – they’re political appointees following political directives.

This matters because monetary policy requires making unpopular decisions. Raising rates during growth periods prevents future inflation but slows current economic activity. Presidents facing reelection want growth and low unemployment, not rate hikes that cool the economy. If the Fed must prioritize presidential political needs over economic stability, inflation becomes inevitable.

What Happened the Last Time Trump Pressured the Fed

During Trump’s first term, he repeatedly pressured Fed Chair Jerome Powell to cut rates, calling him an “enemy” and suggesting he should be fired. Powell maintained independence and made policy decisions based on economic conditions rather than presidential demands.

The result was that inflation remained relatively low (around 2%) and the economy continued growing until the pandemic hit. Trump’s pressure campaign failed because Powell refused to subordinate monetary policy to political preferences.

Trump’s threat to only appoint compliant Fed Chairs represents a lesson learned: if you can’t pressure independent officials into compliance, appoint people who’ll comply from the start. That approach eliminates the independence that protects monetary policy from political manipulation.

If Trump succeeds in appointing a Fed Chair committed to lowering rates during growth periods regardless of inflation risk, the likely result is accelerating inflation that eventually requires much more painful rate increases to control. The short-term political benefit of easier money gets outweighed by the long-term economic damage of inflation spiraling beyond the Fed’s ability to contain it without triggering recession.

The Constitutional Question About Fed Independence

The Constitution doesn’t explicitly address Federal Reserve independence. Article I gives Congress power over money and credit. Congress created the Fed in 1913 through statute and could theoretically abolish it or restructure it through legislation.

But the Fed’s independence from political pressure isn’t just statutory – it’s an institutional norm that protects economic stability. Presidents who threaten that independence risk triggering the very market instability they claim they want to prevent.

Markets trust that the Fed will make decisions based on economic data rather than political pressure. If Trump eliminates that trust by appointing Fed officials committed to implementing his theories regardless of economic conditions, markets will price in inflation risk by demanding higher returns on bonds, raising borrowing costs, and potentially triggering the very market decline Trump claims he wants to prevent.

The constitutional system allows presidents to shape Fed policy through appointments. But it also depends on appointees maintaining enough independence to make unpopular decisions when economic conditions require them. Trump’s explicit commitment to only appointing people who agree with him eliminates that independence entirely.

What Economists Actually Think About Trump’s Theory

Trump’s claim that “Strong Markets, even phenomenal Markets, don’t cause Inflation, stupidity does!” contradicts mainstream economic understanding of inflation dynamics.

Markets don’t directly cause inflation, but the conditions that produce strong markets – high employment, rising wages, increased consumer spending – create demand pressure that can drive prices up if supply can’t keep pace. The Fed raises rates to moderate that demand pressure and keep inflation stable.

Trump’s theory requires believing that the entire economics profession, every central bank in developed countries, and decades of empirical evidence about inflation dynamics are all wrong – and that he’s discovered the secret to unlimited growth without inflation that has eluded economists for centuries.

It’s possible that Trump is right and every economist who studies monetary policy is wrong. It’s also possible that he fundamentally misunderstands how inflation, interest rates, and economic growth interact, and is threatening Fed independence to implement policies that will produce short-term political benefits followed by economic crisis.

The evidence strongly supports the second possibility.